Priya from Hyderabad called us in January wanting to set up a digital marketing agency. She’d already chosen RAKEZ because the website advertised “AED 6,000 licence, most affordable option.” Three months later, she was stuck — Emirates NBD rejected her bank application twice. She ended up with Wio Bank, which charges AED 10 per wire transfer. At 50 international invoices monthly, that’s AED 6,000 per year in bank fees she never budgeted for. If she’d chosen IFZA (AED 2,000 more upfront), she’d have tier-1 bank access from day one. The UAE has more than 40 free zones. Each is run by its own authority with its own activity list, pricing, and banking relationships This guide answers the real question: which free zone is right for your business, and what will it actually cost?

Tax & Compliance 2026: The Earned 0% Status

In 2026, the UAE is no longer a "tax-free" country — it is a low-tax, high-compliance jurisdiction. A free zone is a designated economic area operating under its own commercial framework, offering 100% foreign ownership, customs exemptions, and 100% profit repatriation. Critically, your tax liability is not determined by your licence alone — it is determined by your Economic Substance. For UAE mainland customers, a commercial agent or distributor arrangement is required. But for founders structured correctly, the free zone advantage is significant: qualifying entities can access 0% corporate tax on millions of dirhams in revenue.

| Scenario | Tax Rate | Requirement |

|---|---|---|

| Taxable income < AED 375,000 | 0% | Standard threshold — applies to all companies automatically. |

| Revenue < AED 3,000,000 | 0% | Small Business Relief (SBR) — Must elect in your tax return. Valid until 31 December 2026. |

| Qualifying Free Zone Person (QFZP) | 0% | High-volume traders & service providers with Audited Financials and UAE substance. Income must be "qualifying" under FTA guidelines. |

| Mainland / Non-Qualifying Income | 9% | Any income from mainland UAE customers or Excluded Activities (e.g., banking, real estate brokerage, insurance). |

What It Actually Costs in 2026

UAE Free Zones at a Glance

April 2026 verified data

40+

Free Zones

AED 4,888

Most Accessible License

7d

License Issuance

2000+

IFZA Activities

The 5 Zones Most Indian Founders Shortlist

In 2026 most setup conversations come down to the same five zones. Here’s an honest snapshot of each — including the part consultants often skip.

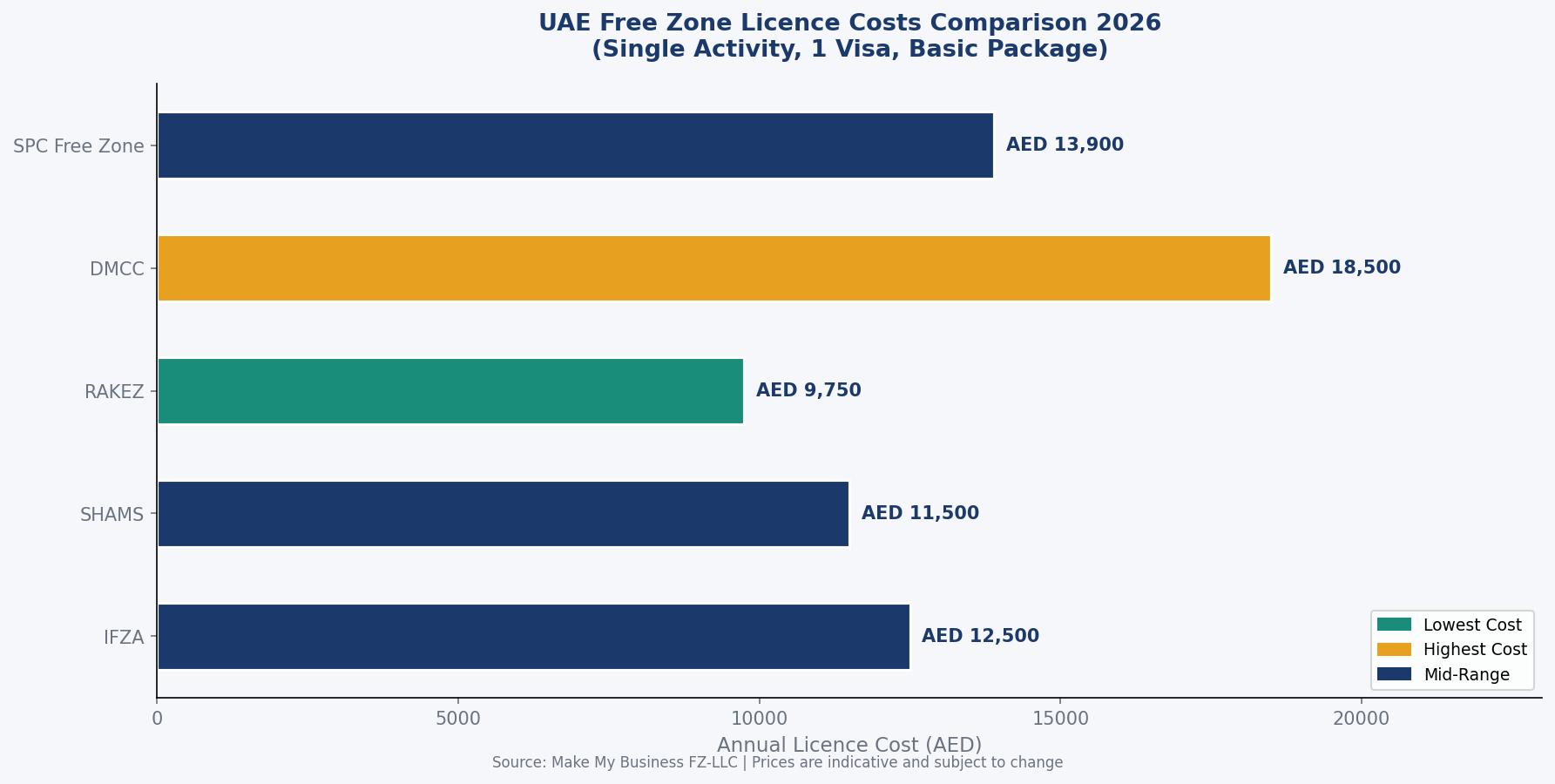

IFZA

INTERNATIONAL FREE ZONE AUTHORITY — DUBAIAED 12,500 license only

Best for: consultants, traders, service businesses. 2,000+ activities. Year 1 all-in: AED 22K–28K.

✓ Tier-1 bank approvedSHAMS

SHARJAH MEDIA CITYAED 11,500 license only

Best for: content creators, marketing agencies, e-commerce. Solid bank acceptance. Quarterly client requirement keeps community active.

✓ Good bankingMeydan

MEYDAN FREE ZONE — DUBAIAED 12,500 license only

Best for: fintech, professional services, brand-conscious consultancies. Premium Dubai address. Banks treat Meydan identically to IFZA.

✓ Dubai addressRAKEZ

RAS AL KHAIMAH ECONOMIC ZONEAED 6,000 license only

Best for: e-commerce, small manufacturing, international export. Cost-effective. Caution: tier-1 banks less enthusiastic about RAK entities.

⚠ Check banking firstSPC

SHARJAH PUBLISHING CITYAED 4,999 from (e-publishing)

Best for: publishers, content businesses, value-focused founders. Digital banks like Wio approve SPC readily. Year 1 all-in: AED 16K–22K.

✓ Cost-optimisedDMCC

DUBAI MULTI COMMODITIES CENTREAED 18,000+ license only

Best for: commodities, gold, crypto. Despite higher pricing, the regulatory ecosystem is unmatched. Compliance is baked in.

✓ Gold standardWhat the Headline Price Excludes

Every free zone advertises a “from AED X” price. That covers the trade licence and a flexi-desk address only. Here’s what you actually need to run a business:

Real First-Year Cost Breakdown (Example: IFZA, 1 visa)

Zone-by-Zone Comparison

| Zone | License From | Year 1 All-In | Bank Acceptance | Best For |

|---|---|---|---|---|

| IFZA | AED 12,500 | AED 22K–28K | ✓ Tier-1 | Consultants, traders |

| SHAMS | AED 11,500 | AED 20K–27K | ✓ Good | Media, agencies |

| Meydan | AED 12,500 | AED 22K–30K | ✓ Tier-1 | Fintech, professionals |

| RAKEZ | AED 6,000 | AED 14K–20K | ⚠ Moderate | E-commerce, export |

| SPC | AED 4,999 | AED 16K–22K | ⚠ Digital banks | Content, publishing |

| DMCC | AED 18,000+ | AED 35K+ | ✓ Premium | Commodities, crypto |

Which Zone for Which Busines

IF YOU ARE A...

Management consultant or service provider (international clients)

→ IFZA or Meydan. Tier-1 bank approval within 3 weeks. Emirates NBD and ADIB approve readily.

IF YOU ARE A...

Content creator, agency, or media business

→ SHAMS or twofour54 (Abu Dhabi). Purpose-built ecosystem for media businesses.

IF YOU ARE A...

E-commerce or trading operator (margin-conscious)

→ RAKEZ or SPC. Accept that you’ll start with Wio Bank and upgrade after 6 months of trading history.

IF YOU ARE A...

Logistics or warehousing business needing physical space

→ JAFZA or DAFZA. Priced higher but built for inventory management and customs clearance.

IF YOU ARE A...

Commodities, gold, or crypto business

→ DMCC. Regulatory ecosystem is unmatched. Compliance infrastructure is built in.

Following the 2024–2025 FATF compliance cycle, UAE banks have materially elevated their Know Your Customer (KYC) and Anti-Money Laundering (AML) thresholds. Tier-1 banks now conduct structured due diligence encompassing your business plan, shareholder CVs, source-of-funds documentation, projected transaction volumes, and customer geography. Certain smaller or newly licensed zones now carry significantly lower approval rates at major banking institutions. An elite advisory firm tracks zone-specific banking approval data as an operational metric — not as an afterthought. If your consultant cannot provide this data, your setup is at risk before it begins.

AML Alert: goAML Registration (2026)

If your business operates in gold, real estate, high-value goods, or high-volume commodity trading, you are classified as a Designated Non-Financial Business or Profession (DNFBP) under UAE AML law. Registration on the goAML portal is mandatory — failure to register before transacting carries significant regulatory exposure. This is not a discretionary obligation.- Renew your licence 30 days before expiry — late fees compound and can trigger account flags.

- Register for corporate tax even if your liability is zero — the AED 10,000 penalty is automatic.

- Maintain an active UAE mobile number on your trade licence — banks use this for KYC verification.

- Keep your flexi-desk or tenancy agreement current — mandatory for visa renewals and banking compliance.

Compliance Architecture 2026: UBO, ESR & Audited Financials

In 2026 these are not optional extras — they are legal obligations with penalties of AED 50,000–500,000. An elite advisory firm briefs you on all four compliance pillars before you sign anything. Licence resellers skip them entirely. The difference shows up in your first banking review.

- Corporate Tax Registration — Mandatory even if you expect to pay 0%. Missing the deadline triggers an automatic AED 10,000 penalty.

- UBO Filing — File your Ultimate Beneficial Owner register within 60 days of incorporation. Update within 15 days of any ownership change.

- Audited Financial Statements — Most top-tier zones (DMCC, IFZA) now require submission via their portals by 31 March annually.

- AML & goAML Registration — Mandatory for businesses in gold, real estate, high-value goods, or commodity trading. DNFBP registration required before transacting.

- Check if your licensed activity triggers ESR obligations (Relevant Activities list).

- Renew licence 30 days before expiry — late fees compound fast.

- Maintain an active UAE mobile number on your trade licence for banking KYC.

- Keep flexi-desk or tenancy agreement current — required for visa renewals and compliance audits.

Request a Zone Strategy Session

Make My Business FZ-LLC are registered channel partners with IFZA, SHAMS, Meydan, RAKEZ, SPC, RAK Innovation City, AFZ, and ANCFZ. As a senior advisory mandate, we provide live zone-specific banking approval data, five-year tax modelling, and QFZP qualification assessments — not generic price comparisons.

This is a strategy session, not a sales call. Come with your business model, expected revenue, and client geography — we’ll come with the data.